[Business] Part 3: Finding the Perfect Investment for 2025

Part 3: Assessing the Industry Environment

Good Morning Readers,

I’m excited for Part 3 (P3) — this is about the point when things become more interesting for me because we start to identify some more nuanced pieces of the puzzle that you would hope inherently generate alpha. The novel ideas, new insights, and piecing together a thesis based on what you see and uncover is sensibly fun.

Part 2 (P2) was all about assessing the macro-environment. Generally speaking, market conditions are favorable for most industries.

In Part 3, I’m going to be going through:

Assessing the Industry Environment

[Part 4 Preview] Understanding Industry Metrics

A side goal of mine is to keep these sections a bit more concise and abstract away the longer thoughts and research as much as possible. I had to split up P2 from P3 because there was so much to talk about, and I don’t want to have to cross that line again.

(P.S. I failed… again! 🤪 )

Ikimashou! 🔥 (Translation: Let’s go!)

5. Assessing the Industry Environment

I briefly poked at this in P2 with regard to how the macro-environment may affect the outlook for our industry, but this part needs to be more granular.

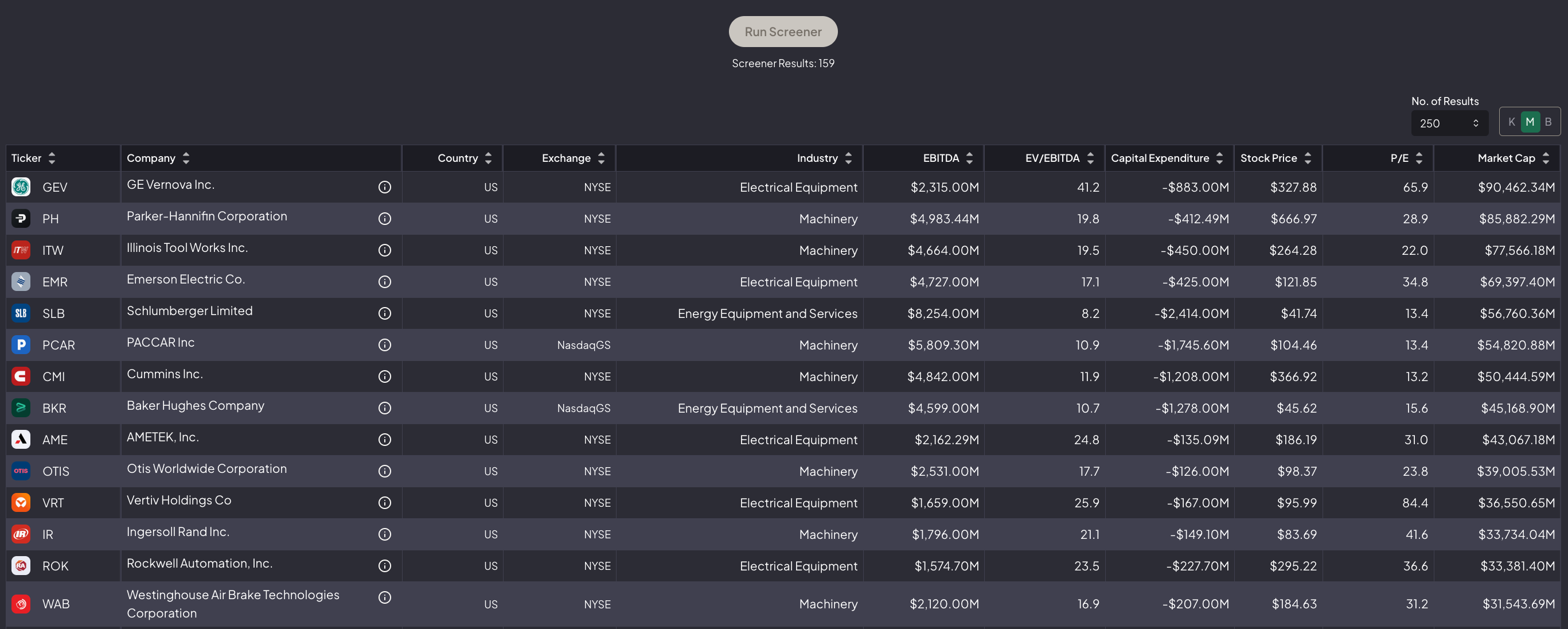

Two ETFs that I have been tracking for awhile now are XLE and NUKZ. XLE offers a more traditional basket of energy picks — natural gas, oil, utility providers, energy infrastructure, etc. and NUKZ offers a tad more risky profile and incorporates what I’m coining a more ‘Energy Enablement’ friendly handful of stocks. For me, these are companies that are developing technologies that will move the needle for the energy industry 1,3,5, and 10 years down the road. Some examples of these are developers of SMNRs (Small Modular Nuclear Reactors), other alternative energy providers in various forms including raw material harvesting, infrastructure, and provider (for spaces such as solar, wind, hydro), and emerging storage and battery technologies.

I track these ETFs to contrast traditional energy with energy enablement trends. To me, this is old wealth vs. new wealth, the David vs. Goliath.

Looking at YTD and 1-Year returns of these ETFs, XLE is up a measly 3.9% and 5.3%, respectively, while NUKZ has gained a 19.2% and 92.5% respectively. Notably, though, but have been experiencing a subtle ramp-up in monthly returns. This tells me that sentiment is generally good for all of energy, and there may even be a larger mega-trend at play with the demand for energy as a whole.

From here, my knowledge of how the Energy industry is really doing was pretty limited. I had my general sense, but it was time to dig deeper.

I started by setting out a list of questions about the industry that I had:

What does the history of the Energy industry look like? How has it shaped our Energy industry today? What are some of the emerging themes and outcomes going into the future?

How is Energy measured? Quite literally, what is one unit of energy called? How do we produce energy? What is traditional energy vs. renewables vs. emerging technologies?

What is the true amount of energy being consumed? Are we meeting demand? What does energy demand look like going into the future?

Who are the major players in the industry traditionally and forthcoming? What makes them different?

What are some industry events to be aware of? How would a CEO think about the current market environment?

What are some key metrics to measure around the energy industry? How do you assess the health or promise of a company in non-financial terms?

To get answers to these questions, I sifted through numerous articles, Youtube videos, podcasts, and had copious conversation strings with different GPTs. Throughout my search a few of my favorite resources were:

The ‘Redefining Energy’ Podcast

‘Energy Evolution’ Podcast

Forbes ‘Energy’ Column

Honorable mention - Reddit (nothing better than aggregating the opinions of people who work in the industry!) 🤖

COOL ALERT - Here’s the link to one of my live Energy conversations with ChatGPT: My Energy Conversation with ChatGPT

Of course, there were many more, but these resources were immensely helpful because they had content spanning over a long time horizon leading up to today. I was able to get ‘caught up’ very effectively.

After spending hours looking into these questions and constantly asking follow up questions to sharpen my understanding, I was able to get a better picture of the industry and could feel my thoughts on everything start to form.

Go Time!

To start, I will say that I was genuinely surprised by how Energy differs from country to country, particularly with policy. While some players have adopted Energy technology quite rapidly and freely (China), others have been very stagnant and slow (Europe), and some seem to still be finding where they fit in that mix (United States).

Along similar lines, it was astounding to find out how dominant China is in the Energy industry. Not only do they provide most of the components that make up the foundation of many countries infrastructure (transformers, batteries, inverters), but they also service those components and infrastructure after the fact. In addition, most of the emerging technology is coming out of China — it does not seem to be the case that they were a ‘first mover’ and that is the only reason why they are on top. One insight that I found interesting related to this is that the Chinese policy towards Energy is very clear - they set out a plan to dominate this space decades ago and so there were no question marks as to how the businesses in China would be affected by future policy, taxes, subsidies, competition, and changing technologies (yes, they pretty much committed to renewables and renewable technology). This is in stark contrast to other nations where there seem to always be question marks around everything, so it makes it hard to steadily choose one route over another from a business standpoint. For example, companies in the USA might have to continuously be asking whether hydrogen, nuclear, LNG, RNG will be supported by the government and that is frustrating when you’re trying to allocate billions in Capex to these technologies.

Before concluding my thoughts on this topic, it is also worth noting that part of the dominance of China in the Energy space can be attributed to their domestic collaboration — they own their entire supply chain. Raw materials providers work closely with energy producers, who get their equipment from Chinese companies, who get it serviced by those companies, who then partner with companies innovating that technology to reduce costs and drive other efficiencies — it is an all hands on deck approach.

So, point number 1: China is dominant and will likely continue to be for quite some time. This is due to favorable industry policy and transparency on behalf of the government. The businesses work together to sustain a positive-sum game within the nation and as a result are even stronger in foreign markets where there is huge money to be made.

Globally, Energy uses and needs are very different — emerging countries like India and Africa aren’t worried about generating clean energy, they’re just worried about having reliable and affordable energy. This is different than more developed countries that have the luxury of looking at alternative energy sources.

Similarly, Energy consumption is a very regional-based thing. Because it is costly to transport almost every energy source across oceans or land, it has to be maintained and produced locally — this means that from an industry viewpoint, you sort of have to establish shop in the region if you intend to do business there, and there doesn’t seem to be a ‘catchall’ company that does this. For example, in the USA, companies regionalize themselves and even label their business operations by state (i.e. business segments of ‘Texas’, ‘Florida’, ‘Pacific Northwest’). This naturally makes one consider how the growth of the area will impact a businesses’ profits now and in the future for that region. On a different note, one key theme that we’ve seen in the Energy industry as of late is Energy requirements datacenters — they are small cities when it comes to Energy. They require their own energy locally (i.e. one datacenter for Meta might require it’s own wind farm nearby). This is important to consider as we look at business segments and who they serve and how. One way to fuse these considerations together is to frame it into a question: “What type of energy will be needed where and for how long?”.

So, point number 2: Energy procurement, production, and consumption is highly geographical and varies greatly by region. New business need (i.e. datacenters) should be considered similarly.

For our investing purposes and time horizon within the USA, the Inflation Reduction Act (IRA) needs to be talked about. The IRA was passed in 2022 by the Biden Administration and it was the largest energy-industry initiative put in place by the US government ever. It emphasized investments in renewables and extended tax credits in a handful of ways to consumers and manufacturers that were involved in the adoption or production of renewables technologies. To keep this short, the Trump administration has very vocally expressed distaste for parts of this legislation and has vowed to retract some of it’s policies. We need to look between the lines with this. Personally, I like some of the policies and dislike others — it’s about the actual legislation, not party affiliation with this. From my research, while Trump does have some executive power to halt ongoing IRA initiatives, lots of them have already taken hold — grants have been handed out, projects have started, and tax credits for certain pieces of the bill have been earned. Furthermore, it seems that only a couple small pieces of this legislation will be targeted heavily — namely, offshore wind and electric vehicles. It doesn’t make sense for any administration to not push for the adoption of domestic energy and also pass additional policy to curb foreign dominance in the space. If you look at the party in power it’s easy to have the idea that traditionally it has been supportive of green efforts, and that’s true, but this isn’t about green or not green, it’s about the larger Energy industry being developed in the US, and from the prior shove with the IRA and desire from the Trump administration to bring Energy production and manufacturing back into the US, I think we can expect a very bullish government sentiment towards Energy.

So, point number 3: Policy within the US doesn’t currently make sense. We are moving to incentivize the wrong things (namely, hydrogen and nuclear too soon) in the near and intermediate term and there is uncertainty as to what stance the nation will take towards its energy. All that said, it makes sense for the US to make substantial positive changes towards its energy infrastructure in multitudes of ways — so I’m willing to bet things will play out as they should.

Lastly, to get a sense of scale for the actual market, it is estimated that the GICS ‘Energy’ market sector has a market cap of 5-6 Trillion. This is around 5-6% of total global stock market capitalization. This doesn’t include Utilities which may be grouped in during our screenings for investing purposes, but assume that our total investible market is ~8T dollars.

And to make understanding the industry by the numbers quick — rapid fire 🔥 :

Global average annual growth — 1.5%

Fossil fuels still account for — 80% — of global energy production. Five companies account for 25% of the total market cap in the traditional Energy space

The renewables market market cap lies at an estimated 2 Trillion dollars. The market cap of the top 5 largest companies make up about 16% of that total market cap

The world is set to add more than 5,500 gigawatts (GW) of new renewable energy capacity between 2024 and 2030, nearly tripling the increase seen between 2017 and 2023. Achieving the goal of tripling renewable energy capacity by 2030 requires a minimum annual growth rate of 16.4% in renewable energy installations

China generated 37% of the world's wind and solar electricity in 2023, with these sources accounting for a record 16% of the country's total electricity generation, surpassing the global average of 13%

And, point number 4: Energy & Utilities are time-tested industries that are at an inflection point in so many ways. There’s loads of strong money involved (reliably backed $), demand is accelerating, methods today are outdated, there are major players — but no company-specific energy dynasty is at hand, and the industries are very tangible to the layman. Emerging technologies are imminent and able to be invested in; there are no established dominant players.

Other ancillary considerations for the Energy industry are events, reports, etc. One event I’m focusing on is ‘CERAweek’ — and perfect timing for our purposes — it is held every year in early March! 🔥 Some key reports include: US Department of Energy (DOE) report, Energy Information Administration (EI) report, OPEC Monthly Oil report, International Energy Agency (IEA) reports.

This next section focuses on my technical understanding of how the Energy industry actually works, so feel free to skip it depending on what your purposes for reading are!

I will mark the end of the technical understanding section with a divider.

Another insight that I had was that Energy production is actually quite interesting. I say ‘actually’, because I wasn’t expecting it to be as creative as it is. I was expecting it to be, “oh, mine coal and frack for oil, say you’re not harming the environment too much, and then get the energy to the consumers”, but I was pleasantly surprised when I learned how this actually works now, some of the creative solutions that are being adopted in different capacities, and ideas for solutions going into the future. Without going into too much detail, the traditional energy generation process via fossil fuels (e.g. oil, coal, natural gas) is actually pretty basic — so that’s nice; you take the fossil fuels, burn it, and then use the dense steam to power an electromagnetic turbine that generates heaps of electrons and directs these electrons to transformers that up-regulate the electric potential of the electrons to be able to then be sent out into the world for certain purposes. Then you have renewables which is where it gets more exciting — this is your solar, hydro, wind, thermal sources where it’s all in the name, ‘renewables’. There is no finite amount of these that can be used, but this energy comes from the source the technology is named after (i.e. solar: the sun, hydro: water, wind: wind 😉 ). This is the space that is being transitioned into currently and while it seems like adoption is rather slow, it has been steadily increase by quite a lot over time. Lastly, we have our emerging technologies: Hydrogen, Liquefied Natural Gas (LNG), and Nuclear (powered by the natural resource uranium). These emerging technologies all have some promise, but they aren’t really adopted in a meaningful way yet; they all kind of have their issues that make it difficult for businesses to really benefit from taking them on. Hydrogen involves the splitting and reformation of water as a compound,LNG is a condensed and high-potential gaseous form of natural gas, and Nuclear energy is made by splitting the the dense element Uranium to generate heat that boils water, which creates steam, and then the process goes on just like traditional energy generation (see above!). One of my favorite Energy production methods not mentioned in any of these three categories is Renewable Natural Gas or ‘biogas’ which is methane captured from landfills and other waste (sometimes, cow 💩 !). I loved learning about how all of these different production methods worked and it’s valuable for our uses here because you start to get a feel for what is truly a viable option today and in the future and what isn’t. You understand how intensive processes are and how that might affect cost from a business stand-point. You get a feel for how new technologies in the value chain (e.g. Fuel Cells, Long-Duration Battery Storage, Grid Management Software) will play into making these overarching processes more cost-efficient, adoptable, and lastly, you start to understand how infrastructure plays a part in this process (e.g. Chinese dominating the transformer, microinverter, and battery industries) and how the need for those components and technologies might evolve with the broader adoption of different energy trends. I would be remiss if I didn’t mention that all of this is wrapped in the ever-fervent blanket of zero and net-zero emissions — none of these technologies can get away from it, and it is a worldwide de facto obligation that companies have to manage environment impact (gross or net) honestly and with care.

Once I got the technical understanding down to a point where I could understand what Energy companies do and how it works (roughly), I was able to look at the industry with a new perspective and understand the landscape a bit more holistically. At this point, I wanted to understand a little bit of scale: how much energy does it take to power a lightbulb, a home, a city, the world? How much energy is needed now and in the future? How much does energy cost to produce (from a monetary and materials standpoint)?

I found that electrical energy is measured in Watt-hours and is measured on a base-10 scale (i.e. each ^1 increment = multiple of 10 = 3 extra zeroes 😃; so, 1 kWh = 1,000 Wh). To start small, to power a 30W lightbulb for an hour it takes 30W x 1Hr = 30 Wh. Okay, groundwork has been laid on this to understand the industry-level scale, which is typically measured in gWh. Copy and pasting piece of my ChatGPT conversation for a quick glance at the scale:

A single home in the U.S. consumes ~877 kWh/month (~10,500 kWh/year).

A large data center may consume tens of megawatts annually.

Transportation fuels (gasoline, diesel, and jet fuel) account for a major portion of daily energy use.

Global energy consumption is estimated at ~176,000 TWh annually.

These numbers are crazy! 🤯

From a cost/raw materials perspective, see my carefully curated ‘Energy Gallery’ below 🤪 :

And with the spot rate of coal being as high as $125/Ton, you start to get a sense for how much of these raw materials we use to power our homes and how much they cost providers.

Now I have handle on all of the ‘ground-work’ — pun intended.

Okay, I put a double-divider above for a reason: time to bring it all together 🔁

What does this all mean from an investment standpoint?

I started this journey by thinking I was going to end up investing in some sort of ground-breaking, earth-leaving, world-changing clean energy technology, and I’m ending my industry research by being much more in the mindset of wondering who is going to dominate the renewables industry and sustain its growth as other Energy tech comes and goes. In a similar light, which companies are key in supporting our existing Energy infrastructure — renewable or other — and perhaps a bit more of a niche side play, who are the innovators in this space?

To explicitly name a few areas I’m watching: grid infrastructure (literal cables, wiring, transformers, etc.), load management technology & software, battery development (specifically Long Duration Battery Storage), commercial wind and solar deployment, and I’m very open to companies with innovative technologies in and a round the spaces listed formerly.

To explicitly name a few areas I’m staying away from: hydrogen, nuclear, carbon capture pure-plays, fossil fuels raw materials extraction, and localized Energy providers.

My research pulled me back to reality which I believe is exactly what happens when you aggregate enough information across the board looking at any investment opportunity.

I really am interested in Chinese companies dominating the space, staying away from Europe (with exception to major, established players), and finding US-based companies that have a strong footprint domestically and could benefit from favorable forthcoming government policy. I really do think it makes sense for the US to be very pro-Energy during this administration, so I think it will be a ‘rising tides lifts all boats’ scenario. In the background, I’ll be on the lookout for how these established companies are imprinting themselves in developing nations.

I’m looking forward to keeping up with industry events and reports throughout this process — CERAweek is coming up, and that will be a great way to get my toes wet. I also will be preparing for future industry reports by reading prior reports to get a sense for where things were trending. I’m excited to keep listening to my new energy podcasts.

I couldn’t help but thinking of the current Energy landscape as a an allegory for US railroads during 19th century and into the early 20th century. Railroads owned the US. They became established and dominated their respective areas of transportation. Their infrastructure was built and became engrained into the landscape of the nation. Then that infrastructure became outdated, new technologies loomed, and the traditional industry failed to innovate. I think parallels can be drawn to how the traditional Energy industry is evolving today. It took 30-40 years for the railroads to fully decline (and even today they are still important for freight purposes), but the technologies that took off in lieu of our RR’s were automobiles, aviation, and trucking — and trust me, you would’ve want to have been an investor on that ride 💰 .

It was amazing to be able to learn so much about such a unique and profoundly creative industry technologically — and consolidating my thoughts to share with you was remarkably impactful on fine-tuning these thoughts to point towards investment ideas.

I hope you took something out of this post, and I’m looking forward to sharing the next pieces in the series!

In Learning,